Disney Bundles Its Way to Success

“Baby Yoda.” These are two words that many consumers have come to recognize, and, frankly, to adore. The surge in popularity of the lovable character is symbolic of the company behind it. During its fiscal Q1 earnings call, The Walt Disney Company reported strong growth for its direct-to-consumer division, which includes Hulu, ESPN+, and newly-launched Disney+.

Disney announced subscriber figures for each of its streaming services for the first time, illustrating its success in the space. Disney+ ended the year with 26.5 million subscribers, claiming its spot as the fourth-largest subscription OTT video service in the US, behind Netflix, Amazon Prime Video, and Disney’s own Hulu (the “Big 3”).

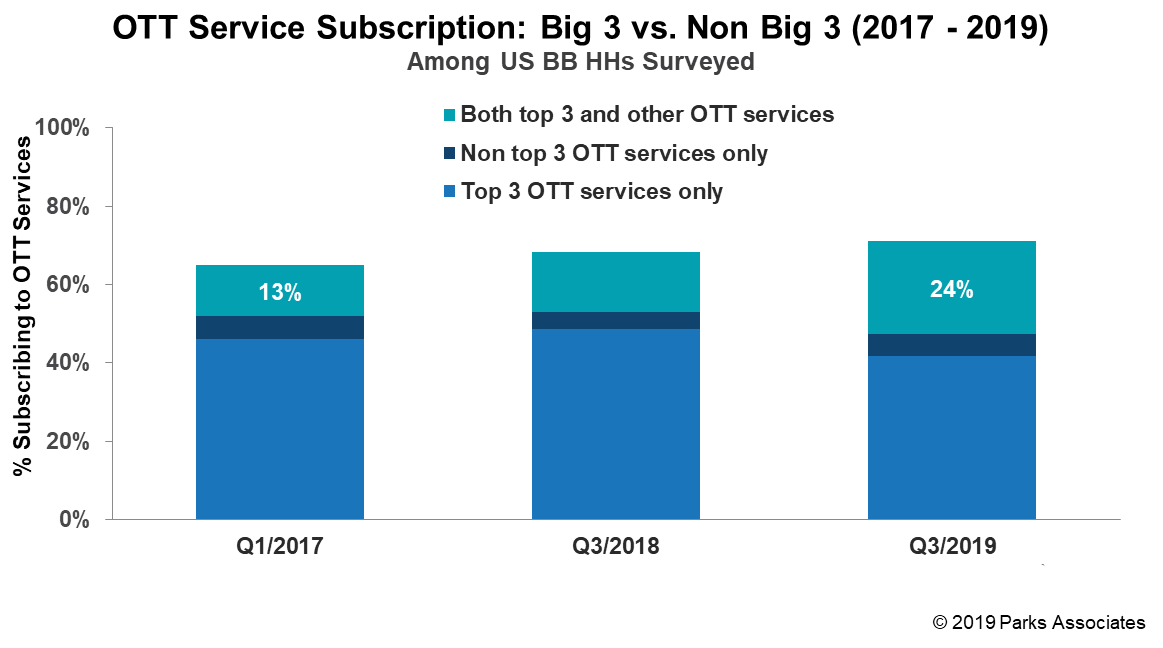

Parks Associates finds that a quarter of US broadband households subscribe to at least one of these services plus at least one other smaller service, nearly twice the amount from two years prior. HBO Now, now the fifth largest service, required over three years to reach 7.8 million subscribers, something Disney+ managed to overcome in its first day. Hulu ended the quarter with 30.4 million total subscribers, with 27.2 million attributed to the SVOD and 3.2 million to its Live TV service. Disney’s third leg of its streaming strategy, ESPN+, ended with 6.6 million subscribers, a tremendous year-over-year growth of nearly 500%. CEO Robert Iger expanded on these figures, stating that Disney+, Hulu, and ESPN+ actually reached 28.6 million, 30.7 million, and 7.6 million subscribers throughout January, respectively. Disney’s ability to grow its subscriber base by millions of subscribers in one month demonstrates the company’s proficiency to effectively reach new consumers.

Disney+’s accomplishment in subscriber numbers is likely due to several factors, including a marketing strategy that goes beyond traditional channels. Among Disney’s assets are theme parks, cruise ships, cable networks, local affiliate stations, merchandise, and two other streaming services - Hulu and ESPN+. Together, these properties touch millions of consumers every day. Disney’s corporate brand is widely recognized and associated with family content.

Where other streaming services rely on promotion of particular content titles or original content, Disney benefits from a portfolio of recognized brands - Marvel, Star Wars, Pixar, and National Geographic. Disney+ was able to attract subscribers despite a limited amount of new original content, in contrast to Apple TV+, Netflix, and HBO Now. Although, exclusive titles such as The Mandalorian (home of Baby Yoda) helped generate its hype. Most of the service’s offering consists of content previously viewed by consumers, with titles dating back as far as 1928. The majority of this content had been placed in a vault, making it difficult to access by consumers in one place. Disney+ essentially opened this vault, providing unlimited access to all of its content – a key driver in its adoption.

Perhaps the largest influence of Disney’s direct-to-consumer success is its distribution strategy. The partnership with Verizon to offer a year free of Disney+ to Verizon’s Unlimited mobile and FiOS home internet customers is what Disney’s CEO credits 20% of the service’s subscriber base. This distribution partnership is a trend that many services have relied on to drive adoption. Disney+ was also offered in a discounted bundle with ESPN+ and Hulu’s ad-supported SVOD plan, which recently expanded to Hulu’s ad-free and live TV options. At its $12.99 per month, this bundle is an enticing offer that includes a well-rounded portfolio of family, sports, and general entertainment content. Consumers essentially receive three services at a price that is lower than Netflix’s Premium Plan or HBO Now. Offering Disney+ in a package with the company’s two existing streaming services enabled Hulu and ESPN+ to significantly boost their subscriber bases.

The Walt Disney Company hopes to leverage this distribution strategy as Disney+ expands internationally. The company signed a deal with France’s leading pay-TV provider, Canal+, and is in talks with various other potential distributors throughout the region, such as Sky in the UK. Iger also announced that Disney+ will launch in India through the company’s Hotstar service, bundling it as a premium tier dubbed Disney plus Hotstar. This distribution strategy augments Disney+’s potential by positioning it in front of Hotstar’s ~400 million monthly active users. Just as Disney’s other US streaming properties benefited from Disney+’s launch, Hotstar is likely to follow.

Disney+’s quick success is reflective of both the shift to and demand for online video. What took leading services Netflix and Prime Video a decade to accomplish Disney managed to do in a couple of months. As the market for OTT video becomes increasingly saturated, upcoming entries HBO Max and Peacock from WarnerMedia and NBCUniversal, respectively, are faced with a new bar for comparative success. Where achieving one million subscribers was once a notable milestone, consumers and industry players will now assess success in comparison to Disney. HBO Max and Peacock will be considered underperforming if they do not significantly exceed 1-2 million subscribers within months of launch.

Parks Associates tracks the robust market of OTT video services, including Disney+, in its OTT Video Market Tracker. Additionally, the evolving dynamics of aggregation and bundling are examined in Parks Associates’ Partnering, Aggregation, and Bundling in Video Services.

Further Reading:

- Avoiding OTT’s Top 5 Mistakes

- 25% of US broadband households use free, ad-based OTT services, and more than 25% are interested in innovative offerings accessed via TV

- The Lifecycle of OTT Video Services - Service Evolution

Next: 360 Deep Dive: Today’s Broadcast TV

Previous: Quibi: The Lush Short-Form Video Platform

Comments

-

Be the first to leave a comment.

Post a Comment

Have a comment? Login or create an account to start a discussion.