New Services Threaten Big 3 in OTT

by

Steve Nason | Jun. 8, 2020

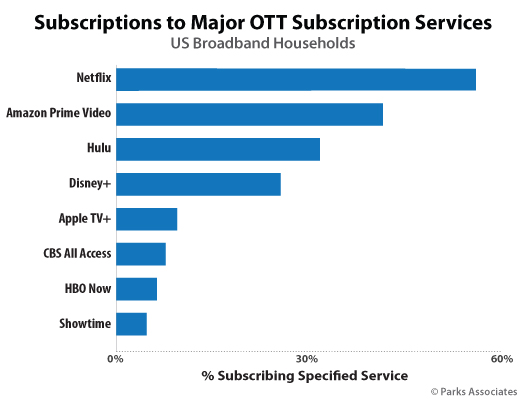

The term “streaming wars” has been used for the past several years to describe the battle between high-profile major SVOD services for ever-elusive revenue and viewership share. However, the “war” up until this point has mostly been fought between the “Big 3 in OTT”, Netflix, Amazon Prime Video, and Hulu. More than 9 in 10 OTT subscribing households subscribe to at least one of those services. While other services have found varying degrees of success, none has truly threatened the hierarchy established by the Big 3. That trend could be about to change.

November 2019 saw the launch of two major OTT SVOD services, Disney+ and Apple TV+. Both took different approaches to launch initially in the market. Disney brought a broad-based aggregator approach to Disney+ with the integration of new and library Disney, Pixar, Star Wars, Marvel, National Geographic, and 20th Century Fox original content into one unified platform. Apple built Apple TV+ with a base of original content from big-name Hollywood names. In the early stages of their growth, both have demonstrated impressive service uptake. According to Parks Associates data from Q1 2020, one-quarter of US broadband households subscribe to Disney+ while nearly one in ten subscribe to Apple TV+, placing these services as the fourth and fifth biggest SVOD services, respectively, after less than six months in the market.

Disney+ and Apple TV+ are not the only services that can threaten the Big 3 in OTT. NBCUniversal’s hybrid AVOD/SVOD service Peacock has already launched to Comcast subscribers with a full launch planned for mid-July. The combination of NBC and Universal content assets and the potential integration of leading ad-supported OTT service Xumo (recently acquired by NBCUniversal parent, Comcast) make the at-launch offering from Peacock rather impressive. The key for Peacock in its quest to approach the Big 3 is to demonstrate the value of the subscription-based tiers to convert users from the free, ad-based tier to paying customers.

Another potential competitor to the Big 3 is WarnerMedia’s SVOD service, HBO Max, which launched in late May. The combination of several Max Originals plus HBO, Warner Brothers, DC Comics, Turner, Crunchyroll and other assets, make HBO Max’s content offering second to none. There certainly will be challenges as WarnerMedia attempts to navigate to the top of the OTT hierarchy. The $14.99 per month subscription cost will make it one of the more expensive SVODs in the market. Also, the unclear future for HBO’s two existing OTT services, HBO Now and HBO Go, add complexity and potential confusion to the consumer buying purchase process. Finally, the existence of those services and other dynamics make negotiations with pay-TV and platform partners much trickier. As the market learns more of HBO Max and the vast library of content it offers, coupled with the planned addition of a lower cost ad-based tier next year, it could very well threaten the Big 3 in OTT in the not-so-distant future.

Finally, ViacomCBS’ expanded CBS All Access offering, which is launching this summer, creating another potential service that can supplant one of the Big 3. CBS All Access is already a very successful SVOD service with several million paid subscribers and a spot near the top tier of services. But, with the integration of additional Viacom assets, the new CBS All Access is poised to ascend even further. The key question for the new service, beyond how it will be branded, is the cost. Starting at $5.99 a month, CBS All Access is currently one of the best values in the OTT SVOD space. However, that is certainly going to rise with the expanded content base and will put the microscope on the value of the additional Viacom assets to subscribers.

These services and others have the potential to dethrone one of the Big 3 in OTT in the near future. However, in order to do so, a service must first demonstrate that the perceived value of its content, user experience, and other aspects of its offering meet or exceed the subscriber’s expectations. The service also has to be deemed a foundational service that is essential for inclusion in a video consumer’s service stack. The severe economic impacts of COVID-19 that have households examining their expenses like never before will also make an ascent into the Big 3 even more challenging.

For a deeper look at the OTT video space, please check out Parks Associates’ OTT Tracker and the Quantified Consumer report Consumer Perception of OTT Video.

Parks Associates also tracks the impact of COVID-19 on consumer behaviors, attitudes, and intentions in the consumer and home technology markets throughout the year through its quarterly trending surveys.

Next: COVID-19’s Impact on Video Consumption: The Smart TV Experience

Previous: COVID-19 and the dramatic increase of video consumption

Comments

-

Be the first to leave a comment.

Post a Comment

Have a comment? Login or create an account to start a discussion.